First thing is, what's the confidence interval around the actual 0.2%? If for example Stats says the number is 0.2%, but plus or minus 0.5%, then there's much less reason for angst over a number that's within the range. I couldn't find any info about a possible confidence interval in the detailed announcement so I got in touch with Stats, who tell me there isn't one (at least not in any formal statistical-theory sense). As a second-best approach, I thought I'd take a look at the historical volatility of the quarterly GDP changes, and here it is.

The upshot is that the quarterly change is quite a volatile beast. Yes, there tend to be strings of positive numbers during a business cycle expansion, but successive quarters are still rather erratic. More formally, the average quarterly change over the whole period is +0.6%, but the standard deviation is 0.8%: if the distribution were anything like normal you'd expect that two thirds of the time the quarterly change would be in a rather wide range between -0.2% and +1.4%. So my quick take is that we ought to keep some sense of calmer perspective about the March outcome.

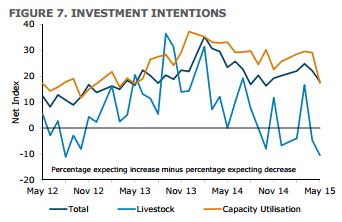

The other thing that seemed strange to me was the -2.8% fall in business fixed investment in the March quarter. The latest ANZ survey, for example, showed that (ex investment in livestock) investment intentions have been running strong by historical standards, as shown below.

But when you unpick the investment numbers, again you get to the same conclusion: there's less to an apparently weak number than meets the eye. There was a surge in investment in plant and machinery and in transport equipment in the September and December quarters of last year: in March the numbers dropped almost exactly back to where they were in June '14 ($9.88 billion compared to last June's $9.84 billion). Look at the numbers in a less volatile way - on a running four-quarters-total basis, for example - and the 'drop' in investment disappears completely.

All up, I'm prepared to believe we're past the peak of the current business cycle - the ANZ survey shows it pretty clearly- but I'm also prepared to believe that the headline March number made things look a good deal worse than they really are.

On the other hand I've also been looking at what's been happening to Australia's GDP: the graph below comes from the Reserve Bank of Australia's excellent Chart Pack, which is a very handy guide to the Aussie macroeconomy.

This looks very much like a gradual long-term deceleration in Australia's growth rate, and at first I thought it might have been due to the winding down of the resource project boom. But the timing is all wrong for that as an explanation: in fact, the mining investment boom did not get properly underway until around 2000, and did not peak until 2012-13. In fact the slowdown in overall GDP growth happened despite the substantial boost to activity from the mining sector.

There's been quite a bit of debate about whether developed countries are looking down the barrel of slower economic or productivity growth in the future: it's been a particularly big issue in the US and UK, where recent productivity growth performance has been very weak. Until I looked at these graphs, I hadn't really expected the Lucky Country to be in the frame as well.

No comments:

Post a Comment

Hi - sorry about the Captcha step for real people like yourself commenting, it's to baffle the bots