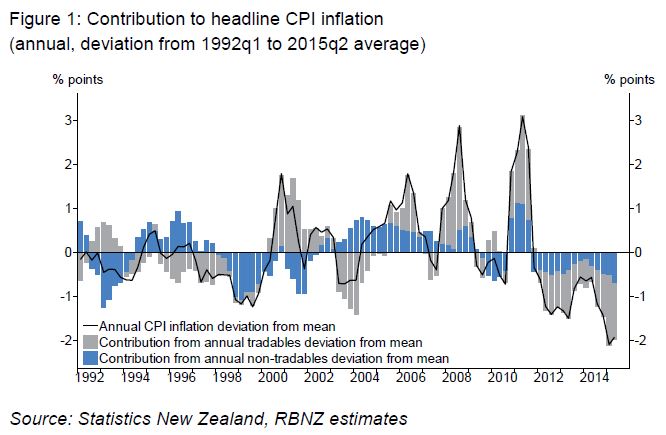

But I would like to expand a bit on the graph below, from the speech, which shows inflation consistently coming in below the Bank's target mid-point in recent years, and which has been fuelling some of the criticism of the Bank - either because its forecasting has been poor, or (hence or otherwise) because it's been running monetary policy too tight.

I'm interested in the blue, non-tradables, part, which is the only bit under our control. It's been lower than usual, and we partly know why (investment in capital equipment and a larger labour force have boosted capacity, so growing demand can be accommodated without inflation). But even after that's accounted for...

Non-tradables inflation has been about ½ of a percentage point weaker on an annual basis than the Bank’s modelling estimates would suggest is normal for this phase of the economic cycle, even allowing for the stronger growth in economic capacity. This underestimate of inflation has also occurred in other countries and could be due to several factors. For example, inflation expectations may be weaker than survey data suggests, the tradables component of non-tradable products and services may be higher than previously thought, or online commerce may be increasing competition and squeezing margins in non-traded sectors, such as retail.I'd love to think that increased competition - from online commerce or other sources - is helping to discipline price increases for our domestic goods and services. That aside, it's clear that both here and overseas our overall state of knowledge about this unusually low inflation is inadequate. Until that gap is filled in, there's the possibility that central banks everywhere may be needlessly on guard against an inflation threat that isn't there.

The real problem, surely, is that if we don't know where inflation has gone we don't know when it will come back.

ReplyDeleteThat's right. I thought at the time about adding a sentence along the lines that, in our current state of ignorance, central banks might as equally be lulled into ignoring a sleeping dragon. Maybe I should have...

ReplyDelete