We kicked off Day 2 with a keynote speech, "The monetary policy remit and two percent inflation", by Adrian Orr, governor of the Reserve Bank, delivered online (full text here or watch the video here) after Adrian came down with a late lurgy (a pity, as I'd looked forward to chewing the fat about the forthcoming NRL season with my fellow Warriors tragic).

|

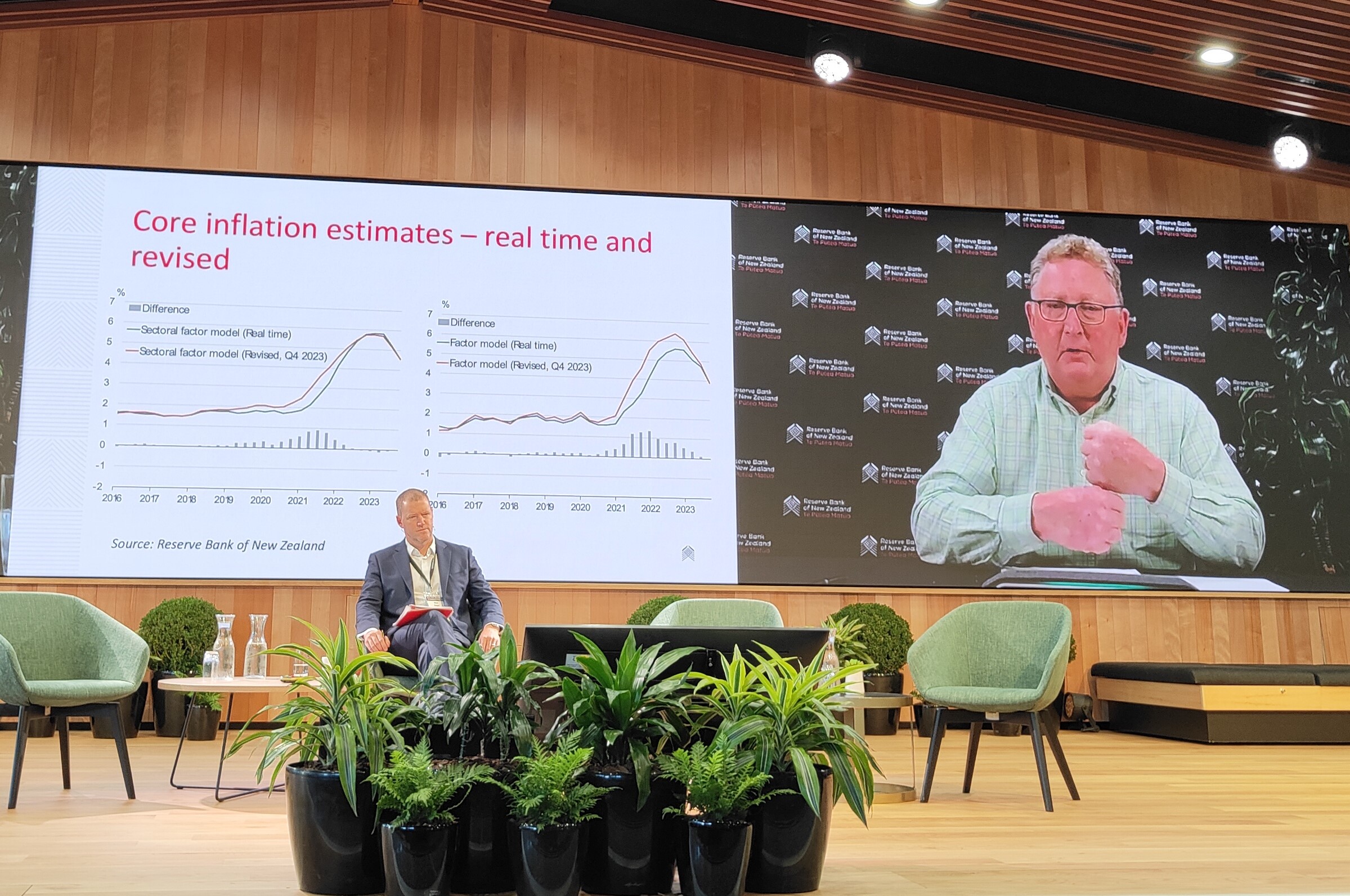

| Adrian Orr with one of his slides, showing that core inflation as it actually transpired over 2020-22 was stronger than the lower real-time estimates available when decisions needed to be made (with Waikato's Prof Matt Bolger as moderator) |

Takeaways? Some sympathy for the RBNZ's (and other central banks') challenges over the past few years: Covid, where Adrian reasonably asked, which mistake did you most want to avoid in the high-uncertainty crisis, and the answer was too-tough policy that might aggravate a downturn, hence the almost universal let-it-rip of both fiscal and monetary policy; the Team Transitory/Team Core debate; the interruption to normalisation from the Auckland lockdown; the Ukraine; and a recent rise in household inflation expectations.

Expectations - which are interlinked with people's trust in the competence of a central bank (what us older folks used to call 'credibility') - look high on the bank's agenda. I noted in the speech that while inflation has come down, "tackling the tail end of these persistent inflation pressures in the domestic economy remains key to achieving 2 percent inflation. Just how persistent these pressures might be depends on how factors, such as capacity pressures and inflation expectations, evolve going forward". Adrian was giving nothing away about the next monetary policy decision (February 28) but if I were in the room I'd be looking at the latest annual non-tradable inflation rate (5.9%) and wondering if those capacity pressures and expectations levels needed a further knock on the head.

Onwards to fiscal policy, first with a keynote from Caralee McLiesh, Secretary to the Treasury, followed by a panel discussion on 'Treasury and the state of the books'.

Caralee's speech doesn't appear to be up on the Treasury website, but you can get the gist of it from the excellent 'Economic and Fiscal Context Slide Pack' which was part of Treasury's Briefing to the Incoming Minister of Finance. A key point was that our fiscal deficit is structural, not cyclical: as Caralee said, it tends to be easy to loosen fiscal policy in a downturn, and a lot harder to wind back the spend in better times, and we've now reached the point where belated policy tightening is needed (we'd got the same message from Nicola Willis the previous day). "Difficult distributional decisions lie ahead": quite.

|

| Treasury Secretary Caralee McLiesh speaking to our rise in net public debt |

The 'State of the books' panel - Craig Renney from the CTU, Eric Crampton from the New Zealand Initiative, Sarah Hogan from the New Zealand Institute of Economic Research - may have been intended to have been a battle of "duelling economists", as one person put it, but it turned out to be a lovefest of harmony and mutual understanding which coalesced around the theme of the importance of getting the best value for money from the public spend.

As Craig said, there's nothing inherently "right-wing" in demanding value for money and nothing inherently "left-wing" in spending the right amount. Sarah pointed to health as one area where we are not getting value for money: Pharmac (she said) may take its lumps from its critics, but on the other hand it is a rare example in the sector when it comes to revealing its prioritisation. Other areas are either not transparent, or may not even prioritise in the first place. Eric would like us to retreat from the post-Covid spending bloat, perhaps to the same share of GDP that the Wellbeing Budget of 2019 represented (core crown spending of 29.1% of GDP, compared to the 33.0% expected for 2023-24 in last year's Budget forecasts): one reason was that people would be less likely to sign up to future rainy day spendups if they see previous ones sitting there unpaid for. And all the panellists were very keen on a really rigorous framework of prioritisation and evaluation: as Craig put it, "Think hard, and then think hard again".

|

| The "duelling economists": Craig Renney, Eric Crampton, Sarah Hogan, with (on left) panel moderator Waikato's Prof Anna Strutt |

Then we got a panel on 'Infrastructure: Unclogging the arteries', a topic close to my and I'd guess every other New Zealander's heart, given the increasingly shabby state of virtually all the infrastructure we use, from hospitals, classrooms, and roads to those infamous three waters. I drove down to Hamilton from outside Warkworth. The good news is that Warkworth to the approaches to the Harbour Bridge went fine (thanks to the new Puhoi motorway extension, even if it took forever to build), and Drury to Hamilton was fine (thanks to the new Waikato Expressway, also remarkably protracted). The bad news was that the intervening Harbour Bridge to Drury stretch remains an absolute nightmare, undoing a fair amount of the Puhoi/Waikato benefits, and the throttleneck looks like staying that way for some considerable time. There's a huge deferred bill looming: one speaker mentioned the Infrastructure Commission's estimate that we will need to spend $30 billion a year for the next 30 years.

Alison Andrew, CEO at Transpower, told us that while the current transmission grid is in good shape, (a) most of it was built in the '50s and '60s and is getting to its use-by and (b) there's an opportunity to green the country through electrification, but we will need 22 gigawatts of generation (and associated transmission) compared to today's 10 gigawatts. She didn't say it, but I personally wondered why the Commerce Commission regulates Transpower in 4-5 year bites, rather than over a longer-term horizon. Chris Joblin, CEO at Tainui Group Holdings, said it wasn't so much unclogging the arteries that's needed, but more like a double or triple bypass after being on the fags since the '70s: we just haven't being looking after our infrastructural health. And when we do bestir ourselves, the consenting takes forever: he mentioned that it took 17 years to get Tainui's inland port at Ruakura (just beside Waikato University, as it happens) up and running. Among the issues: we look for perfection, which causes procrastination, and we load too many objectives onto projects, blowing out the costs and causing further rethinks. And Nick Leggett, CEO at Infrastructure New Zealand, agreed that we need to get our project management process right: we can occasionally rise to the occasion but mostly we're bad at it.

In passing, if the planning and project mismanagement omnishambles gets your goat, too, you'll like Daryl McLauchlan's piece for Democracy Project, 'Unjarndycing the State'. And if you'd like a piece on how we might do better, here's one I prepared earlier for Acuity magazine, 'Getting results'.

Life's too short, so I'll just pass briefly over the final two sessions. 'Climate & Weather: So what happens if we don't curb emissions?': answer, bad stuff, and for some of the same reasons that our infrastructure record is so poor. As Sir Brian Roche said, we make a virtue of recovery from disasters, but we don't provide for preparedness in the first place. If 'value for money' was a recurring theme of the Forum, 'dynamic inefficiency', not investing enough to keep the show on the road, ran it a close second.

And in 'Fintech Futures: The end of cash?', no, cash is not dead, with the RBNZ's Karen Silk reminding us of why we still use it (full and final settlement, in privacy, plus benefits when, say post-Gabrielle, the ATMs and EFTPOS go down). And on the fintech side, we've had some successful financial innovation - we heard from Brooke Roberts, co-CEO of one of the successes, Sharesies - and while Brooke hoped that we will eventually have a global fintech come out of New Zealand, it's generally not as easy to get things up and running as it is in, say, Australia. Shane Marsh, cofounder of DOSH, also wondered about us falling behind. In my mind, I've always thought of New Zealand as a digitally advanced place - we were using EFTPOS for everything when our friends and rellies in Ireland, the UK or the US were still writing cheques - but the world's moved on, and we haven't. In Shane's view, our payments landscape is now well behind the rest of the world and even behind some of the 'developing' world .

Matt Bolger, Pro Vice-Chancellor of the Waikato Management School, sent us on our way with an uplifting message. While it's tempting to think that today's rate of change is unprecedented, Matt said we shouldn't get so up ourselves: how do we compare, really, with the generations who went through the Great War, the Depression, fascism and communism, and World War Two? And despite our current inability to plan properly for tomorrow's challenges, maybe he's right that we shouldn't get overwhelmed, and we should stay optimistic. It would be nice to think that New Zealand Economic Forum 2025 will be able to document that we're getting more of a grip on the issues that face us.

No comments:

Post a Comment

Hi - sorry about the Captcha step for real people like yourself commenting, it's to baffle the bots